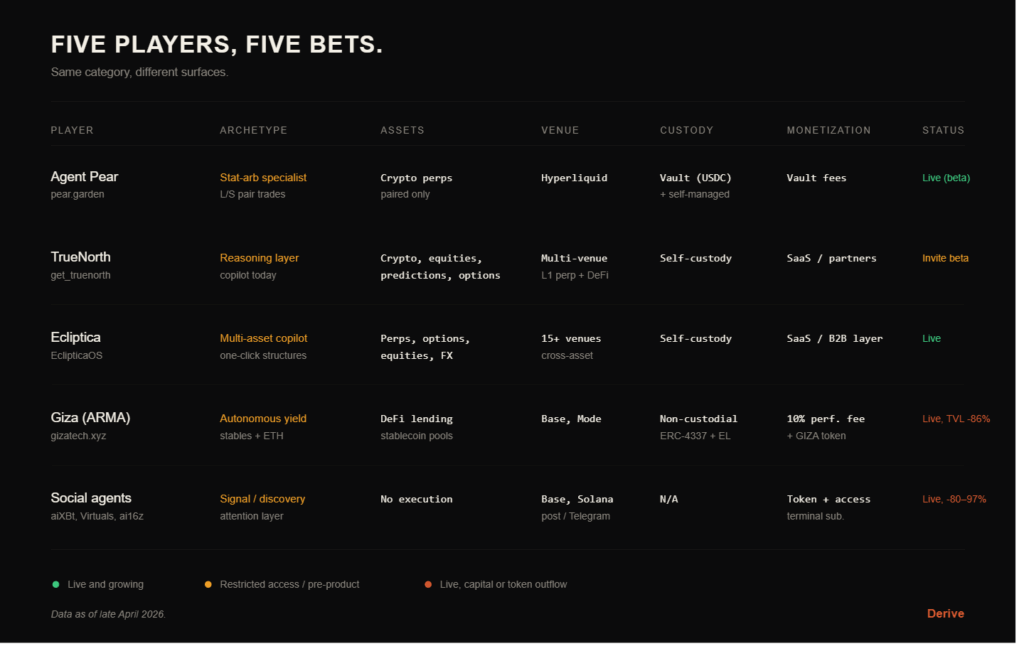

Five players, three working categories, one cautionary tale. We looked at where agentic trading actually stands in April 2026: what works, what still has to prove itself, and which bets are being made right now.

The Quiet Inflection

Most crypto narratives announce themselves. Agentic trading hasn’t. And yet somewhere in late 2025, executing trades through a language interface stopped feeling like a demo and started feeling like an actual workflow. A non-trivial share of the volume on Hyperliquid is now driven by software that decides for itself what to do next. This trend most likely will continue.

The category contains a wide spread, from tools that meaningfully change how a trade gets entered, sized, and managed, to social mascots that recycle Twitter sentiment into ticker form. Lumping them together is the standard mistake of every “AI agents in crypto” piece.

This article picks five anchors that, between them, cover the actual surface area of the market right now. Agent Pear, the stat-arb specialist whose beta we got hands-on with. TrueNorth, the institutional bet on domain-specific financial reasoning. Ecliptica, the multi-asset copilot. Giza, the AgentFi benchmark whose token chart now tells a more complicated story than its product. And the social agent layer (aiXBt, Virtuals, ai16z), which operates on completely different mechanics from the first four.

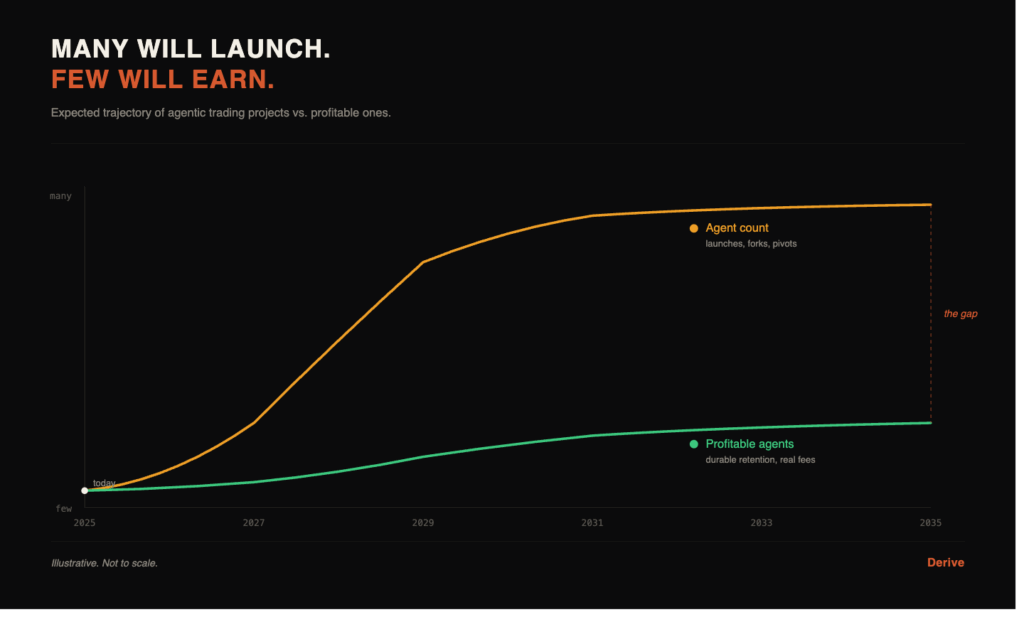

The underlying thesis: agentic trading is one of the rare narratives in crypto where the product surface is measurable. Agents either trade well, or they don’t. Vaults either earn, or they don’t. Telegram messages either save you a click, or they don’t. That makes the next 24 months unusually clean to evaluate. By the end of 2027, two or three of the names below will look like the foundations of a real category. The rest will most likely look like 2021 NFT marketplaces.

Agent Pear: The Stat-Arb You Can Talk To

We opened a HYPE/ASTER pair trade through Agent Pear’s chat last week. Telegram, plain English, no dashboard. Over the following days we tracked it the same way, with a few short messages, a custom monitoring rule, and updates whenever the pair moved.

A typical exchange went like this. Update me on my HYPE/ASTER trade; how is it going? I see the market is pulling back in general.

It came back with a chart and the relevant numbers in plain text. Price ratio at 61.53 against an entry of 61.02, unrealized PnL up about 1.15%, take-profit target still far away at a ratio of 88, no stop-loss set. Then a sentence in normal language: the market had pulled back, but the pair was still in profit, and did we want to adjust TP, add a stop, or change monitoring frequency?

We replied: Just monitor it, give me an update when the chart swings 3% or more in any direction. It set up the monitoring task, returned a task ID, and confirmed it would only ping on a 3% move in either direction, checking hourly.

The whole exchange took two minutes. Across the week, the agent handled position monitoring without us touching a trading interface once. This is what agentic trading feels like when it works. Not full autonomy, not set-and-forget, but a conversational copilot that meets you on the channel you already use. Super helpful, especially if you’re not able to access your usual environment while traveling e.g.

Founder @hufhaus9 recently showed all current features in a short form video accessible on X:

The product underneath the chat is more serious than the interface suggests. Agent Pear evolved out of CryptoWizards, a stat-arb tool from earlier cycles that gave traders correlation tables and z-score charts but stopped at analytics. The Pear team rebuilt the full statistical library (Pearson correlation on log returns, dynamic beta against structural beta, ADF tests for cointegration, Monte Carlo thresholds tuned for crypto rather than equities) and added two things CryptoWizards never had: real-time alerts when a z-score compresses past a threshold, and direct execution on Hyperliquid. The monetization will sit in a future vault model. Depositors put in USDC, and the agent runs pair trades within pre-set risk parameters.

Those stats are among the best and most consistent results with a decent track record in the whole space.

What makes Pear interesting in the agent context isn’t the stat-arb math. Pair trading has existed since LTCM. It’s the interface layer. A trader on the move can ask the LLM to surface live divergences, pull in data from CoinGecko or velo.xyz inside the same chat, and open or adjust positions without ever loading a trading terminal. That collapses the distance between seeing a pair diverge and acting on it from minutes to seconds.

The honest limitation is scope. Pear does one thing. If you want yield, directional perps, or memecoin sniping, this is not the product. But the focus is also the bet. Pair trading is a mature, well-understood strategy that benefits from automation and 24/7 monitoring far more than from human discretion. Agent Pear is what happens when someone takes that obvious match seriously.

TrueNorth: Building Finance-Specific AI

Last week, Delphi Labs co-founder Jose Maria Macedo (@ZeMariaMacedo) flagged something unusual about agentic trading. The structural point: non-crypto AI trading startups are raising at $200 to $300 million caps even pre-product or with weaker offerings, while comparable crypto-native teams cannot reach those numbers from VC alone. TrueNorth in particular, he argued, has built one of the strongest products he has seen in the category anywhere. He called 2026 a “generational opportunity” to back crypto-native teams building products with universal appeal. Standard caveat: Delphi led TrueNorth’s pre-seed alongside Cyberfund, GSR, Bryan Pellegrino, and Jordi Alexander. The man has skin in the game. But the structural claim is independently verifiable. Non-crypto AI trading startups are pricing at multiples that crypto-native teams cannot get to. If true, that is a pricing anomaly worth understanding.

TrueNorth is built by Willy Chuang and Alex Lee (previously involved in WOO X and research time at Intel). The premise they build on is bleak. ESMA’s 2018 product intervention measure, based on regulatory analyses of CFD trading across EU jurisdictions, found that 74% to 89% of retail accounts lose money, with average losses ranging from 1.600 to 29.000 EUR per client. Caveat: that figure is specifically about CFDs, not retail trading writ large. Chuang stretches it. But even adjusted, the picture is the same. People keep showing up, and most of them keep losing.

The volume side underscores how big the addressable problem is. The gap between participation and competence is widening, not narrowing.

The product is structured around what Chuang calls the Agentic Curve, a three-stage progression for how trading interfaces evolve from human-led to agent-led.

Stage one is Copilot. The trader leads, the agent accelerates. Charts, scans, risk checks, key levels surfaced instantly. The agent runs in parallel and surfaces what the trader would otherwise have to find manually.

Stage two is Surrogate. The agent leads, the trader sets boundaries. Strategy is encoded once, then the agent runs the playbook across all assets continuously, rebalancing and adjusting risk in real time. The human is no longer in the seat but still holds the harness.

Stage three is Autopilot. Full autonomy within parameters. The agent reasons, acts, and reports. Liquidation defense, strategy adaptation, 24/7 execution at a scale no human can monitor.

TrueNorth is currently at Stage one. The beta has a waitlist of over 40,000 users, internal benchmarks claim 98% accuracy on finance-specific tasks against general models, and 30-day retention sits at around 33%, roughly double industry averages. The Q2 2026 roadmap promises coverage of 360 assets, real portfolio management, and execution through both a leading L1 perpetual venue and DeFi spot infrastructure. Q3 is when the Surrogate stage is supposed to come online.

The longer thesis is more interesting than the near-term product. Chuang’s endgame is not tools for human traders. It is becoming the infrastructure layer that other agents rely on to operate in financial markets. The framing in his writing: agents are your hands, but they need eyes and a brain to navigate. The bet is that general-purpose LLMs will not be good enough at finance specifically, and that whoever builds the domain-specific reasoning layer ends up owning the picks-and-shovels position in agentic finance.

Two honest questions remain. First, the company is at Stage one of its own three-stage curve, with most of the differentiated value living in Stages two and three. The roadmap is ambitious, and 13 people is a lot to ask for full-coverage execution across crypto, equities, commodities, prediction markets, and options inside two quarters. Second, the central thesis (general models will not be good enough at finance) is implicitly a bet against rapid LLM progress. That bet has not paid off for many specialized AI startups in other verticals, where general models eventually swallow the specialized ones. TrueNorth has to stay ahead of that curve while building on top of it.

For now, what they have shipped is a Copilot. That is exactly what their roadmap promised for this stage. Whether it scales to Autopilot is the question Chuang is openly betting his company on. Status quo can be seen within @ColdBloodShill latest morning view, probably sponsored by TrueNorth: https://x.com/ColdBloodShill/status/2049068396092801471

Ecliptica: The Multi-Asset Copilot

If TrueNorth is the institutional bet on a single domain done right, Ecliptica is the bet that retail traders want one tool to handle everything they already do across venues. Same copilot framing, but spread across asset classes the average crypto-native trader rarely sees in one interface: perps, options, equities, FX, futures.

The pitch on the product side is concrete. A multi-modular AI scans more than 200 markets continuously and surfaces what matters in real time, with alerts via Telegram, email, or in-app. A second module called AI Profiles reviews the user’s full portfolio and trade history, looking for edge, leaks, and Sharpe-driven performance insights, then recommends adjustments. Notifications are shaped to the user’s stated style rather than a generic alert template.

The interesting layer is the one-click structures. Funding arb, iron condors, spreads, strangles, delta-neutral. The AI builds the structure, the user approves, the platform handles the legging and the cross-venue execution. This is the part of trading where retail traders historically lose the most time and make the most mistakes, sizing legs wrong, missing fills on one side of a spread, mismanaging Greeks. Ecliptica’s bet is that compressing that workflow from twenty minutes to one click is where the real value sits.

There is also an “autonomous execution layer for funds and trading teams” mentioned on the site, sitting on top of what they call Strata signals, pitched as mandate-aligned deployment for B2B clients. That is a different business than the retail copilot, and the public information on it is thin.

What makes Ecliptica worth covering alongside TrueNorth is the philosophical contrast. TrueNorth is building a finance-specific reasoning layer that may eventually serve agents directly. Ecliptica is building a venue-agnostic execution layer that compresses workflow today. Same end state (the agent does most of the work) approached from opposite directions.

Giza: When the Product Outruns the Token

If Pear, TrueNorth, and Ecliptica are the bullish chapters, Giza is the cautionary one. Not because the product failed, but because the market lost faith faster than the product could prove itself.

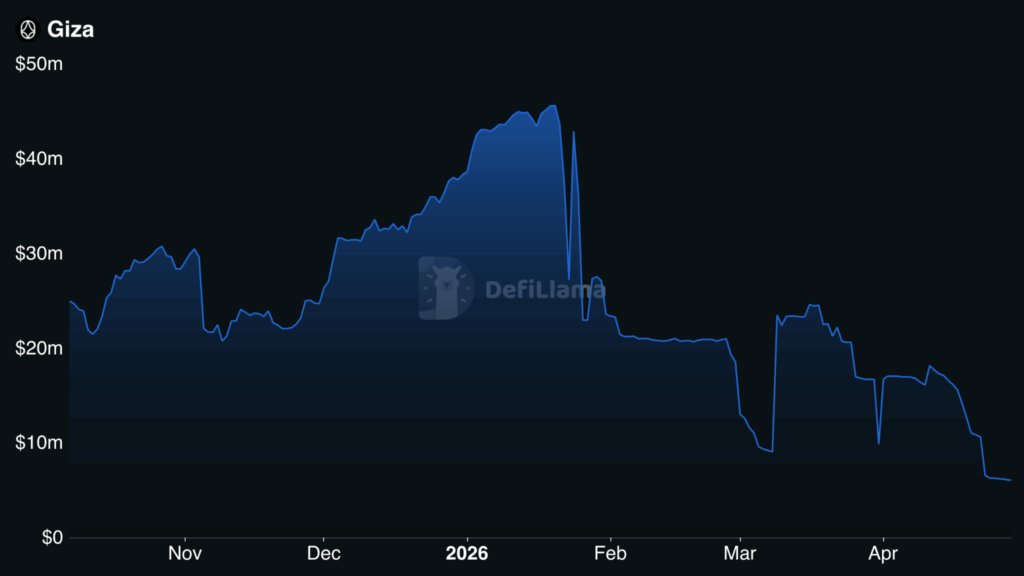

ARMA was the first agent in the category to look genuinely production-ready. Non-custodial, built on ERC-4337 smart accounts with EigenLayer-backed staking and session keys, it monitored lending markets across Base and Mode and reallocated stablecoin deposits to the highest-yielding pool, automatically. By mid-2025 it had processed over 100,000 transactions, managed more than $32M in user assets, and posted backtested yield improvements of 67% on stables and 18.5% on ETH against static allocation. In May 2025, Re7 Capital deployed $500,000 USDC into ARMA, the first institutional pilot for an autonomous agent in DeFi. That was the high-water mark of the AgentFi narrative.

Since then this happened:

TVL peaked at roughly $45M in early 2026 and is now at $6.07M. A drop of about 86% in two months. The product kept running. Fees actually went up. But the capital walked.

Several things probably drove it. The token unlock schedule got brutal in Q1, GIZA traded to deep discounts, and the broader AgentFi narrative cooled as headlines moved on. Some of it was rational rotation. ARMA optimizes lending yields, and lending yields on Base and Mode compressed hard in early 2026, so the absolute return for staying in the agent dropped, even if it still beat passive. Some of it was reflexive. When the token bleeds, the protocol bleeds, even when the underlying mechanics still work.

The lesson is not that Giza is broken. The product is still live, still non-custodial, still doing what it claims. The lesson is that being the AgentFi benchmark in 2025 did not protect Giza from being the AgentFi cautionary tale in 2026. Token-incentivized TVL is fragile. Yield-following capital is even more fragile. Both moved at the first sign of better opportunity elsewhere.

Social Agents: Selling Attention, Not Execution

Social agents are the loudest and most-followed players in the category, but they do not trade. They do not manage positions. What they sell is attention, framed as alpha. aiXBT by Virtuals is the archetype: an AI agent that scans crypto influencers, on-chain flows, and news, then posts synthesized signals on X and Telegram. Token-gated terminal, premium tiers, the works. Performance has been weak across the cohort, with most social agent tokens trading 80% to 97% below their January 2025 highs.

The deeper problem is structural, not cyclical.

First, signal quality is hard to verify. Hit rates get published by the agents themselves with heavy selection bias. There is no audited track record, no reproducible benchmark, no way for a user to know whether the calls that worked were skill or survivorship. The signals are also public, which means whatever edge exists evaporates the moment enough people act on it.

Second, the line between sentiment and fact gets blurred in ways that have real consequences. During the HYPE team-token unlock period, social agents repeatedly amplified posts that mixed verified on-chain unlock data with X commentary about supposed unlocks that were not actually happening. The aggregation layer did not distinguish between the two, and the resulting “signals” moved positions for users who took them at face value. This is the failure mode of an agent that consumes Twitter as ground truth: it inherits whatever Twitter believes, including the parts Twitter is wrong about.

Social agents can have genuine value as an aggregation layer that compresses fragmented narrative into something readable. The mistake is treating that aggregation as an execution edge. It is a discovery layer, and a noisy one. Anyone trading on it should price it accordingly.

Comparison

Five players, five different bets on what an agent should be. Pear is the specialist. TrueNorth and Ecliptica are the copilots, approached from opposite directions. Giza is the autonomous-yield benchmark and the cautionary tale at the same time. Social agents sit one layer removed from the rest.

Zooming Out

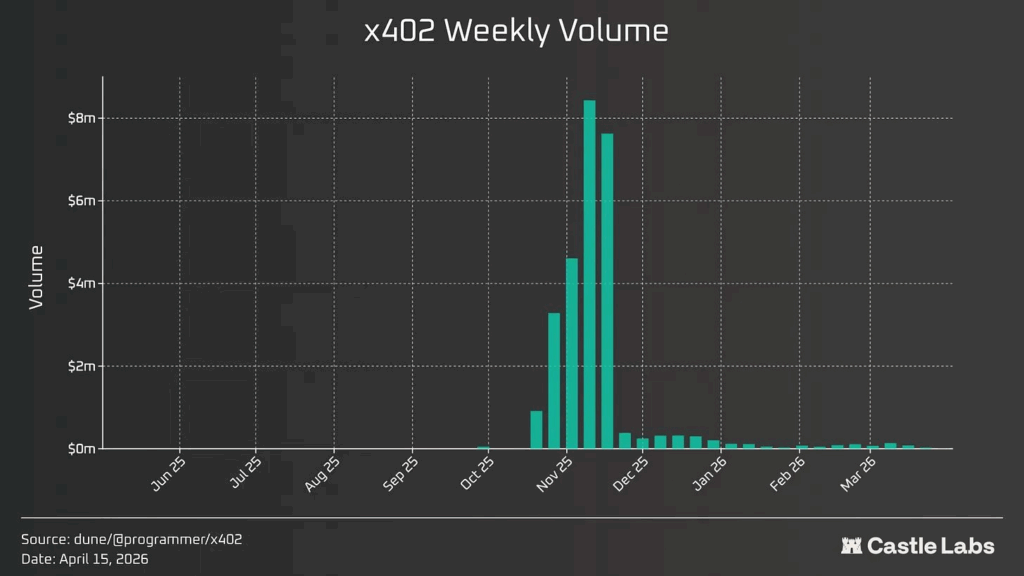

The pattern from Giza is not unique to one product. Coinbase’s x402 payment rails for agent-to-agent transactions peaked at roughly $8M in weekly volume in late November 2025 and have since collapsed to marginal levels, with most weeks now barely registering on the chart. Lifetime volume sits around $48M, almost all of it concentrated in that Q4 spike.

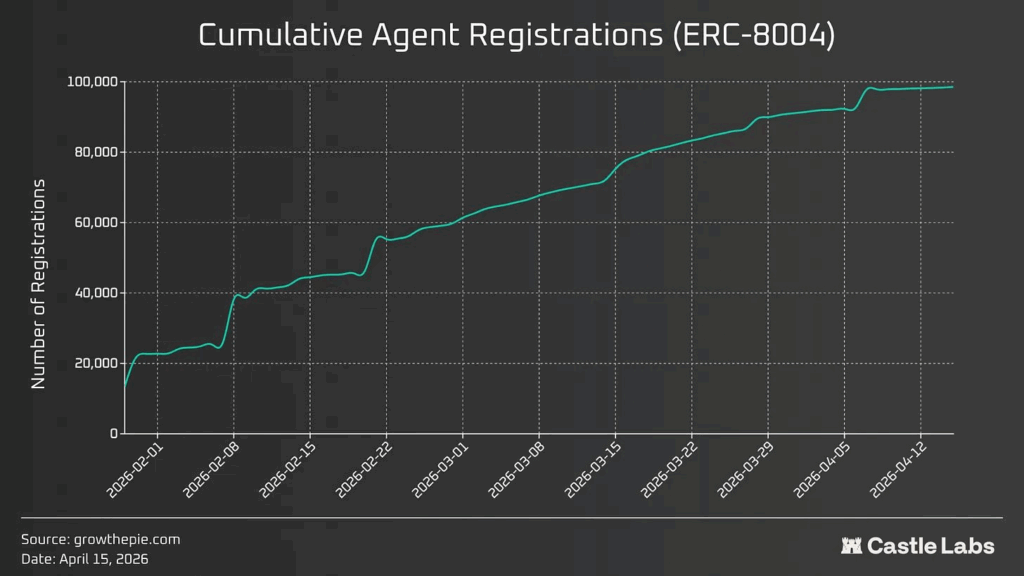

The standards layer is moving the other way. ERC-8004, the agent-identity standard live since late January 2026, has crossed roughly 98,000 registrations across 10+ EVM chains in under three months, on a curve that has stayed remarkably steady. Read together, the two charts mark out the actual signal in the noise. Speculative volume retraces, identity infrastructure compounds. The category is maturing on the rails, not on the headlines.

What to Watch

Two things matter more than the rest of the noise.

Hyperliquid as the execution layer. Agent Pear runs on Hyperliquid. TrueNorth’s L1 perp partner is widely assumed to be Hyperliquid. Senpi, Wayfinder, and a long tail of other agents do too. The combination of Builder Codes, which share revenue with whoever routes the order, and HIP-3, which allows permissionless market creation, is becoming the default agent infrastructure in crypto. Whatever you think of the chain, it is where the agents are landing.

The open question is geographic. Hyperliquid still has no US perpetuals license, which means the entire American market, where AI development sits furthest ahead and where the most sophisticated agent builders are concentrated, is structurally cut off from the venue most agents are being built on. That gap can resolve in two ways. Either Hyperliquid finds a regulated US path and becomes the obvious global execution layer for agentic trading, or a US-compliant venue captures the American agent flow and the market splits along jurisdictional lines. The outcome shapes which teams in this report still matter in 24 months.

Vault-as-product. The cleanest business model in the category right now is a vault that takes user deposits, runs a strategy, takes a fee, and reports performance on-chain. Pear has it. ARMA has it. Hyperliquid native vaults have it. The model is verifiable, custody-aware, and aligned with the user.

Both threads are big enough to carry their own report, and we will most likely come back to each of them separately. For now, the takeaway is narrower. The agents are arriving.

A Prediction, Loosely Held

Two tentative bets, held loosely.

Conversational copilots like Agent Pear seem well positioned to capture a slice of the retail and prosumer trader market that already lives on its phone and is used to managing positions through chat interfaces rather than terminals. Whether that translates into durable market share depends on execution, but the surface fit is real.

On the vault side, it feels like a question of when rather than if agent-operated vaults on Hyperliquid start to stand out, and some of them may turn into profitable, repeatable strategies over time. That is not a prediction that most will work. Most probably will not. But the infrastructure is in place, the incentives are aligned, and the category is young enough that the standout cases have not been written yet.

Disclaimer: Of the products covered, only Agent Pear was tested hands-on. All other assessments are based on public information, team materials, and on-chain data as of late April 2026. None of this is financial advice.

This article was created in cooperation with Derive Insights.

Leave a Reply